#会计准则#国际会计准则

中国会计准则与国际会计准则的差异

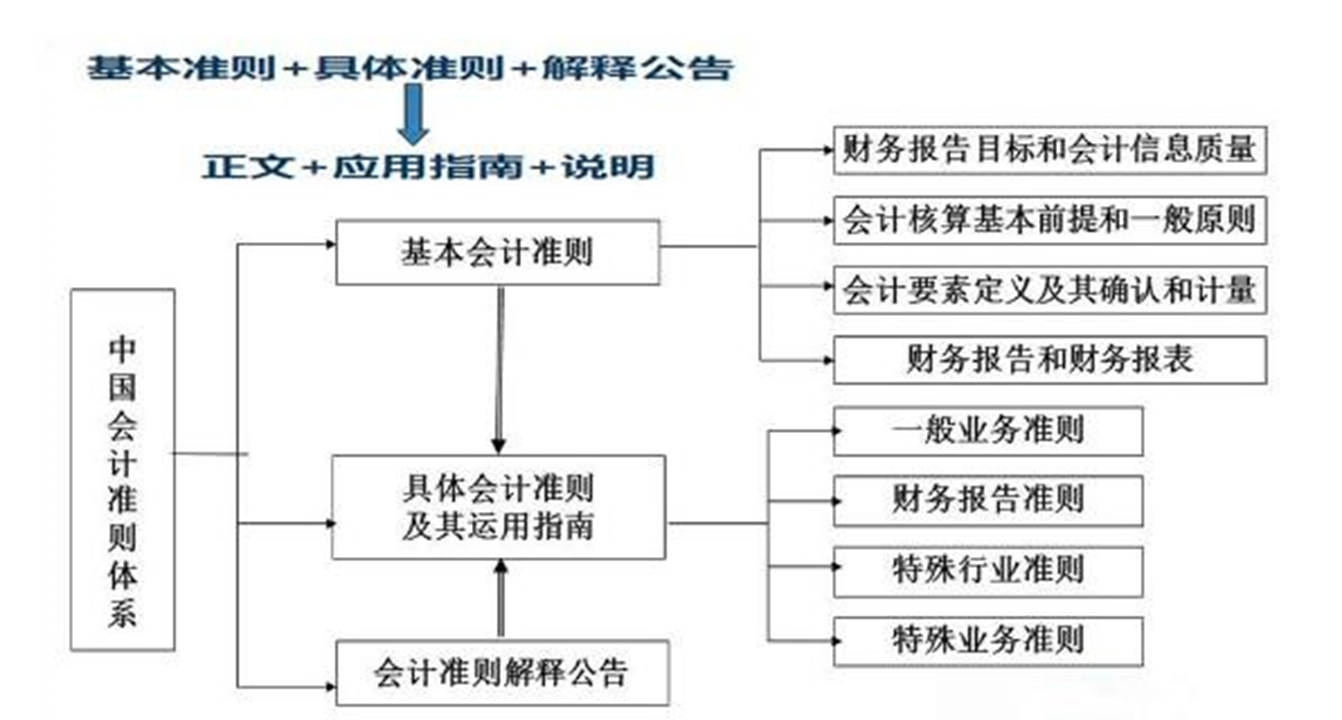

中国《企业会计准则》

- 背景和目的

- 中国境内的适用性和重要性

国际会计准则(IFRS及IAS)

- 背景和全球适用性

- 在国际金融报告中的重要性

IAS是International Accounting Standards 的缩写,意为“国际会计准则”。指2001年前颁布的旧准则。

IFRS是International Financial ReportingStandards的缩写,意为"国际财务报告准则" 。指2001年后颁布的新准则。

都是由国际会计准则理事会(IASB)发布和维护的全球通用会计准则体系,但存在一些区别。

1.差异-框架结构

- 中国会计准则以“基础”为核心 rulebased framework

- 国际会计准则以“框架”为基础 Principles-based framework

Principles-based framework

The purpose of the IASB's conceptual framework,is to assist the IASB in the preparation and review of IFRS, to assist auditors in forming an opinion on whether financial statements comply with IFRS, to assist in determining the treatment of items not covered by an existing IFRS.

The accruals basis and the underlying assumption(going concern)are the basis of the conceptual framework.

Fundamental qualitative characteristics : relevance(nature and materiality)/ faithful(complete,neutral,free from error) Enhancing qualitative characteristics: comparability/verifiability/timeliness/understandability

https://xueqiu.com/1756343398/166219320

2.差异-制定者

中国企业会计准则的制定者是中国会计标准委员会(ASB)。ASB是中国财政部设立的专业标准制定机构,负责制定和发布中国会计准则。

国际会计准则的制定者是国际会计准则理事会(IASB)。IASB是一个独立的全球专业会计标准制定机构,负责制定和发布国际财务报告准则(IFRS)。

ACCA是:

国际会计准则委员会(IASC)的创始成员

国际会计师联合会(IFAC)的主要成员

1999年2月联合国通过了以ACCA课程大纲为蓝本的《职业会计师专业教育国际大纲》,该大纲将作为世界各地职业会计师考试课程设置的一个衡量基准。

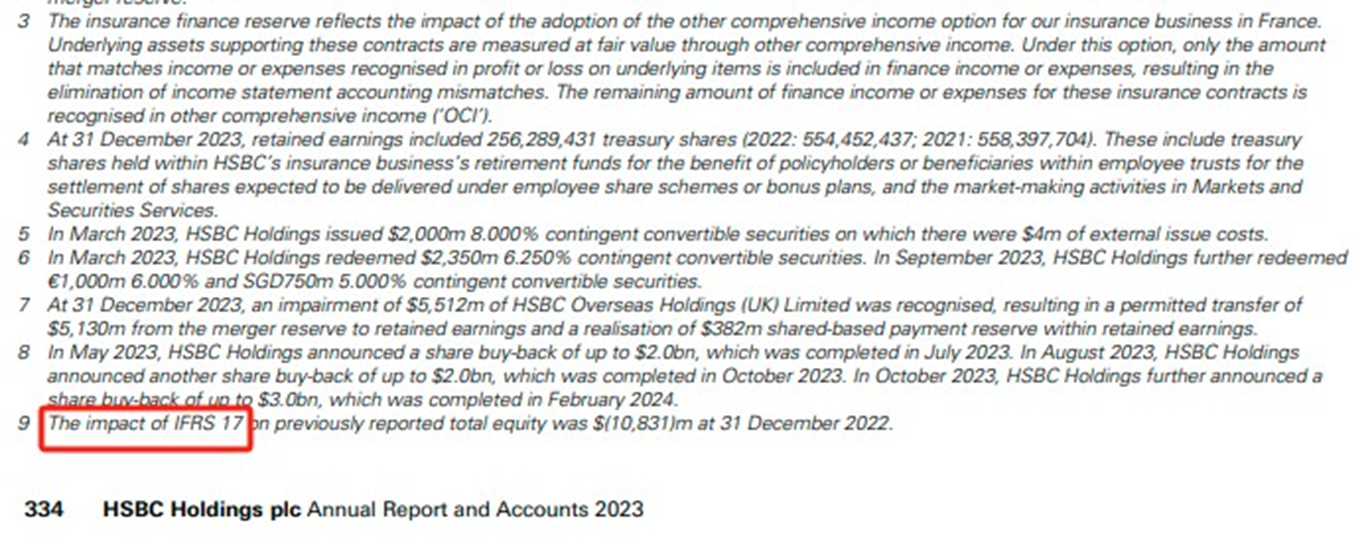

汇丰银行年报遵从国际会计准则

3.差异-资产和负债会计处理

中国和国际会计标准在资产和负债会计处理方面,存在差异。比如:资产重要性测试和计价模式、负债分类依据和租赁合同处理等

4.差异-收入和成本费用

中国和国际会计标准在收入和费用会计处理方面,存在差异。包括:收入确认时间点、成本费用资本化。

例:研发费用资本化

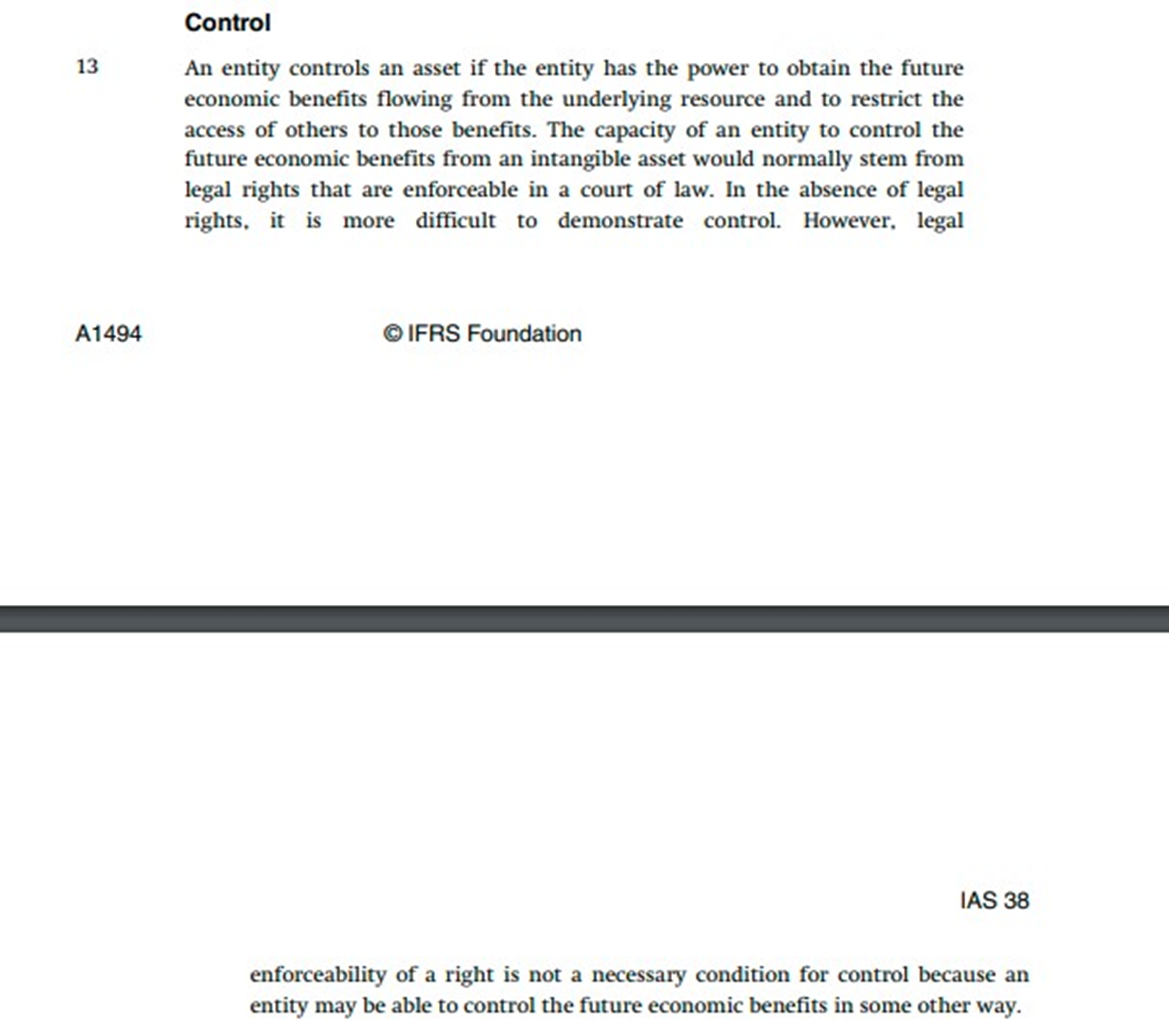

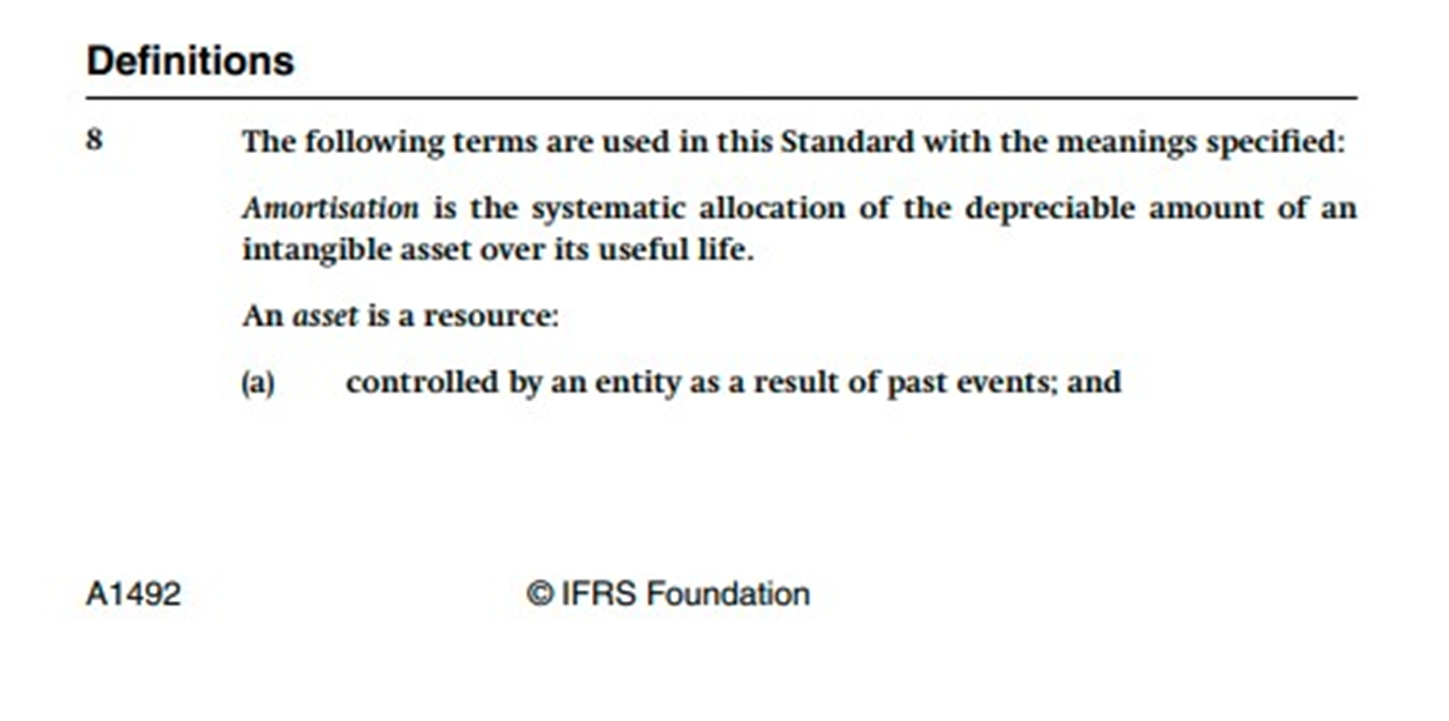

中国会计准则第6号和国际会计准则IAS38都允许企业将符合条件的开发阶段研发费用资本化为无形资产,并在未来的期间进行摊销。

国际会计准则又特别强调:控制

5.差异-报告要求

包括报告格式披露要求和附注内容的差异。

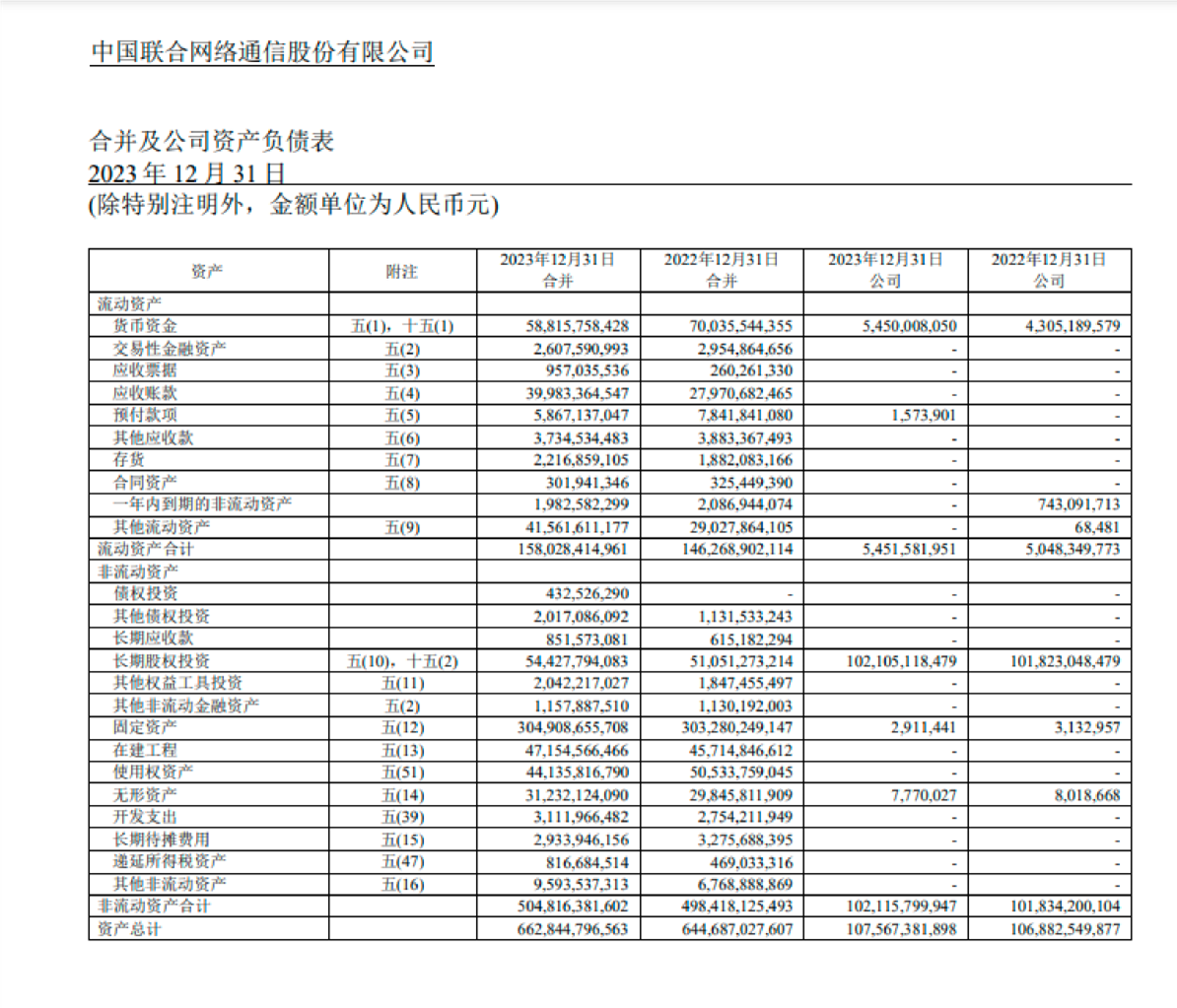

中国联合网络通信(香港)股份有限公司 港股762

哲学思辨

Philosophical speculation is the practice of critically examining fundamental questions about

knowledge, existence, values, ethics, and the nature of reality. It involves rigorous inquiry, logical reasoning, and abstract thinking to explore complex concepts and ideas.

----AI

- 不同语言带来不同

- 语言是思维的镜子:底层哲学思想不同

结论

参考文献

International Financial Reporting Standards. (2021). IAS 38 Intangible Assets. Retrieved from https://www.ifrs.org/content/dam/ifrs/publications/pdfstandards/english/2021/issued/part-a/ias-38-intangible-assets.pdf

ACCA Global. (n.d.). Research and development. Retrieved fromhttps://www.accaglobal.com/gb/en/student/exam-support-resources/fundamentalsexams-study-resources/f7/technical-articles/rd.html

ACCA Global. (n.d.). Research and development. Retrieved fromhttps://www.accaglobal.com/gb/en/student/exam-support-resources/fundamentalsexams-study-resources/f7/technical-articles/rd.html#:~:text=Under%20IAS%2038%2C%20an%20intangible,use%20or %20sell%20the%20asset

China Unicom. (n.d.). Reports. Retrieved from https://www.chinaunicom.com.hk/sc/ir/reports.php

中国通信服务股份有限公司. (n.d.). 投资者关系. Retrieved fromhttps://www.chinaccs.com.hk/sc/ir/ir.php

HSBC Holdings plc. (n.d.). Annual Report. Retrieved from https://www.hsbc.com/investors/results-and-announcements/annual-report

Ministry of Finance of the People's Republic of China. (n.d.). 企业会计准则. Retrieved from https://kjs.mof.gov.cn/zt/kjzzss/kuaijizhunzeshishi/

关于我们

答税科技是由立信合伙人发起创立的高新技术企业,依托专业财税专家团队,采用互联网、云计算和大数据等技术,为企业及个人提供全方位财税服务和产品。

答税微信公众号

客服企业微信

© Copyright(C)2018 © Copyright © www.webtax.com.cn, All Rights Reserved.深圳答税科技有限公司

粤公网安备 44030402006125号

粤公网安备 44030402006125号

暂时还没有讨论信息